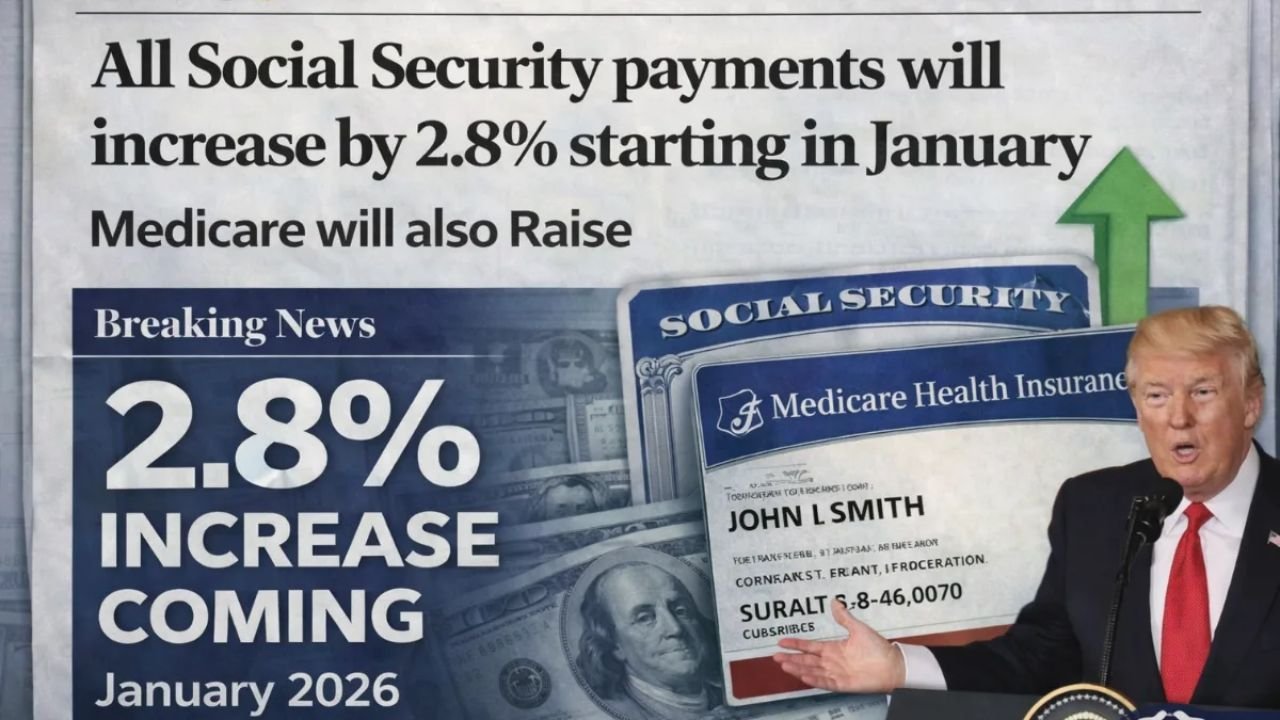

For over 70 million Americans relying on Social Security or Supplemental Security Income (SSI), January 2026 brings a welcome boost. Monthly benefit checks have increased due to the annual Cost-of-Living Adjustment (COLA), a legally mandated change that applies automatically to retirees, people with disabilities, and survivors.

With grocery prices, utilities, healthcare, and everyday essentials remaining high, even a modest increase can make a meaningful difference. For those on fixed incomes, the COLA acts as a safeguard, helping benefits maintain their real value and easing the pressure of rising expenses.

What the Cost-of-Living Adjustment Means

The COLA is not a bonus or special legislative payment. It is a permanent feature of the Social Security system, designed to protect beneficiaries from inflation. When prices rise faster than income, purchasing power declines—but the COLA ensures benefits keep pace.

Each year, the Social Security Administration (SSA) reviews inflation data to determine the adjustment. When costs increase, benefits are raised accordingly, keeping payments aligned with real-world living expenses.

How the COLA Is Calculated

The COLA is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). The SSA compares price data from the third quarter of one year with the same period in the following year. If prices have risen, the COLA is applied to Social Security and SSI benefits.

This calculation focuses on everyday costs—food, housing, transportation, and medical care. Because it follows a strict formula, the adjustment is independent of political decisions or budget negotiations. Benefits rise only when inflation data indicates increased costs.

How Your Monthly Benefit Changes

The COLA is applied as a percentage increase to your current gross monthly benefit. Higher benefits see larger dollar increases, even though the percentage adjustment is uniform.

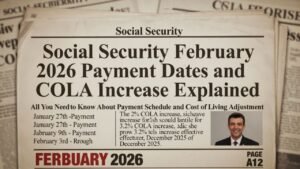

For Social Security recipients, the January 2026 payment reflects the December benefit adjusted for COLA. SSI recipients see the increase applied directly to their January payment. The update happens automatically—no forms or applications are needed.

Why This Increase Matters

For many, Social Security is the primary source of income. Rising rent, utilities, and healthcare costs make even small monthly increases important. The COLA helps reduce financial strain, allowing beneficiaries to cover essentials without resorting to credit cards or delayed payments.

Impact Beyond Retirement Benefits

The COLA affects more than retirement checks. SSI payments, including maximum federal amounts for individuals and couples, also increase. This ensures that low-income Americans are not left behind as living costs rise.

Medicare Part B premiums are impacted as well, but the hold harmless provision prevents premium increases from reducing net Social Security benefits for most retirees when the COLA is smaller than the premium hike.

Working While Receiving Benefits

Beneficiaries who continue working before reaching full retirement age benefit from higher earnings limits aligned with inflation. This allows part-time or supplemental work without reducing benefits, providing additional financial flexibility.

Planning Wisely With the Increase

Although the COLA is automatic, using it strategically can improve financial stability. Many beneficiaries prioritize essential expenses first—covering rising bills or household needs. Others allocate funds to pay down high-interest debt or build emergency savings, which can ease future financial shocks.

Even modest adjustments can add up, helping cover medical costs, home repairs, or unexpected expenses over the year.

How to Confirm Your New Payment Amount

No action is required to receive the COLA. Beneficiaries can verify the updated amount by logging into their online Social Security account, where official notices and payment details are available. Checking records ensures accuracy and aids in planning for the months ahead.

Looking Ahead

The annual COLA underscores Social Security’s long-term purpose: to protect income against inflation. While it may not solve every financial challenge, the January 2026 adjustment reinforces the program’s reliability as a stable, inflation-protected foundation for millions of Americans.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or retirement advice. COLA percentages, benefit amounts, and program rules may change. Readers should consult the Social Security Administration or a qualified financial professional for guidance specific to their individual situation.